Prajwal Pandey is one of our 2020 winners for the HIEEC.

The coronavirus pandemic has changed our society forever, particularly in terms of the global economy and markets. This essay explores the economic effects of the ongoing pandemic and the necessary policy work needed to counter these effects.

Impact on Markets and Economies

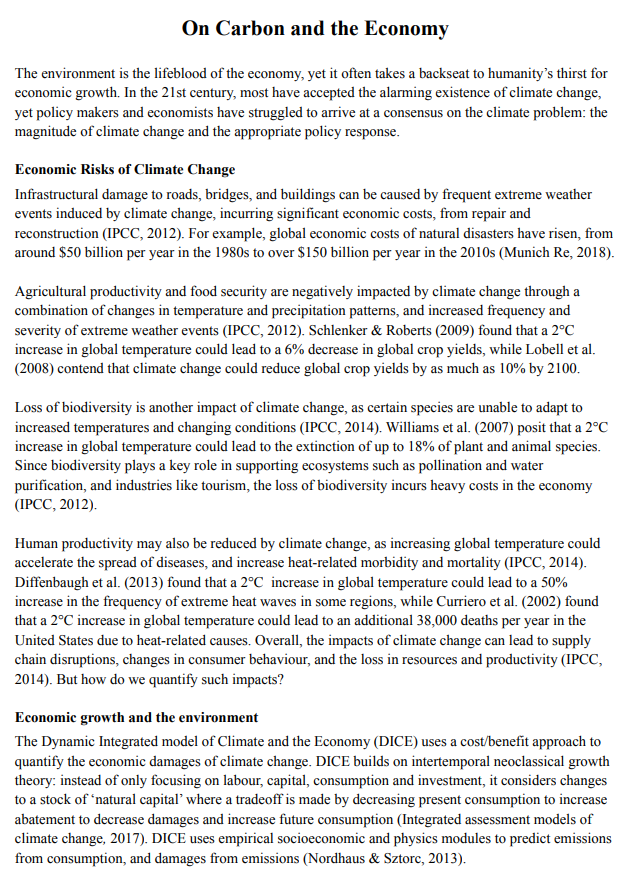

Conventional wisdom conveys that this pandemic has had negative effects on markets and economic growth. This is due to lower disposable incomes and propensities to consume on the demand-side, as well as supply chain shocks and draconian lockdown measures forcing businesses to shut on the supply-side. This has culminated in a $9 trillion short-term global loss in cumulative output. However, long-term effects may differ. To visualize the long-term impact of the pandemic on growth rates, consider a standard Solow-Swan neoclassical growth model.

Key growth factors in this model have suffered over the coronavirus pandemic. For example, population growth rates (n) have decreased internationally, as is exemplified in the US, where population growth is expected to be at its lowest in over 100 years. Additionally, technological innovation (g) has suffered. This is because FDI inflows, that help finance innovation, have reduced by 49% globally, and the openness to trade ratios of economies have been damaged by recently implemented protectionist policies, thereby disabling the efficient cooperation of economies for innovation. Nevertheless, the effects of this on the steady-state output equilibrium is nullified by increases in savings rates (s). Households have been saving a higher proportion of their disposable income for the long-term, due to the increased economic uncertainty created by the pandemic. This is exemplified in the UK, where the savings ratio of Q2 2020 is 20.6% higher than that of Q2 2019, culminating in higher levels of investment being financed, thereby growing total new capital stocks. Assuming that depreciation rates remain constant, this will ensure that output levels remain relatively unscathed.

Many may argue against this inference using Keynes’ Paradox of Thrift; if autonomous saving rates increase then there will be a decrease in consumption and aggregate demand, thereby decreasing economic growth and total savings. However, this argument ignores Say’s law; supply creates its own demand, meaning that as savings, capital stock and supply increase, decreases in aggregate demand will be offset. Additionally, as banks have more funds for lending through increased savings rates, lending by commercial banks will increase, leading to consumer disposable income increasing. Hence, aggregate demand will be sustained. This is demonstrated in the US, where consumer credit increased by 4.4% and 2.1% in September and October respectively, corresponding to increases in consumer spending by 1.3% and 0.3% respectively. Thus, as this savings-driven effect continues in the long-run, the negative effects of other growth factors will be retracted.

Therefore, we can illustrate this dynamic on the below Solow-Swan growth diagram. Adjusting the relevant variable functions from baseline, the long-run output equilibrium decreases only fractionally. Therefore, despite initial deterioration in markets and economic growth in the short-term, global output levels and markets will remain relatively unaffected after the pandemic is resolved.

Contrary to initial assumptions that the universality of the pandemic will lead to more egalitarian societies, this pandemic has worsened labor market inequality. Low-income workers have found their hours and wages cut to a greater proportion than their high-income counterparts (as much as times as much in the UK for example). This is due to low-wage workers typically having lower marginal revenue products than their higher-paid and skilled colleagues. Hence, firms make these low-ability workers redundant before higher-skilled workers to maintain productivity. To approximate the macro effects of this on income inequality, we can observe the effects of previous pandemics on the Gini coefficient of countries. Modeling the income distributional effect of pandemics by estimating the impulse response function (the dynamic reaction of the Gini coefficient) directly from local projections is the log of the distribution variables (the Gini coefficient) for country i in year t, and is responsive to variables such as time fixed and country fixed effects. Empirical estimates, utilizing said model, have conveyed increases in both market and net Gini coefficients of 0.75% to 1.25% 5 years after pandemics on average. When adjusting for heterogeneity in the effects of pandemic events on economic activity, estimates for the current pandemic’s effect on the global Gini coefficient increase to as much as 2% due to the severe economic contractions over several episodes of the pandemic. This estimation is consistent with that of the IMF, which has estimated the Gini coefficients of emerging market and developing economies to potentially rise to 42.7% (around the same level as 2008). Thus, it can be seen that inaction of governments on this matter will see the reversal of all the improvements in labor market equality all across the world since the 2008 recession.

Furthermore, wealth inequality has intensified due to the coronavirus pandemic. Utilizing Piketty’s famous r>g hypothesis*, we can analyze the mechanism underlying this increase. Drastic increases in capital gains (r) for wealthy business owners and stakeholders has been signaled by the S&P 500 index closing at a record high of $3,389.78 6 months after the genesis of the coronavirus plunge in markets. Contrastingly, global GDP per capita has decreased by around $690 from 2019 to 2020, indicating severe decreases in economic growth (g). Hence, trends of deepening wealth inequality, accelerated by the coronavirus pandemic, are evident.

Policy Proposals

Evidently, sound policy work is needed to counter the economic stress of the coronavirus. It is vital that fiscal policy facilitates the ensuing market recovery. Furthermore, it is critical that existing redistributive mechanisms, specifically taxation and welfare benefit spending, are enhanced to counter the negative effects of the pandemic on labor market inequality.

Thus, governments should increase taxes for greater budgetary revenue accumulation for redistribution, whilst still minimizing potential distortions to the ensuing economic recovery. Considering that income taxation is the primary source of revenue for most governments, we can look to optimal income tax theory to inform policy recommendations. Working from an elasticity based model, economist Emmanuel Saez has controversially called for a top marginal tax rate (τ) of 71% for maximizing revenue accumulation without compromising economic efficiency or aggregate productivity.

However, Saez relies on compensated and uncompensated labor supply elasticity being controversially as low as 0.2 for the 71% estimate. Economists have argued that this greatly underestimates the total deadweight loss of such a high tax, due to behavioral effects like shifting income into non-taxable forms and tax evasion being unaccounted for.

.....

篇幅有限,扫码即可免费获取完整版论文pdf